David Beckworth directed me to an attention-grabbing debate at a latest Brookings panel. Olivier Blanchard and Ben Bernanke offered a paper that evaluated varied elements within the latest inflation surge, highlighting the function of provide points associated to meals, vitality, shortages, and many others. To be clear, they famous that among the provide bottlenecks occurred as a result of earlier over-stimulus of demand. Additionally they argued (accurately for my part) that inflation strikes from transitory to everlasting when it turns into embedded extreme wage development. The preliminary inflation surge was excessive costs relative to wages; the present drawback is extreme wage development.

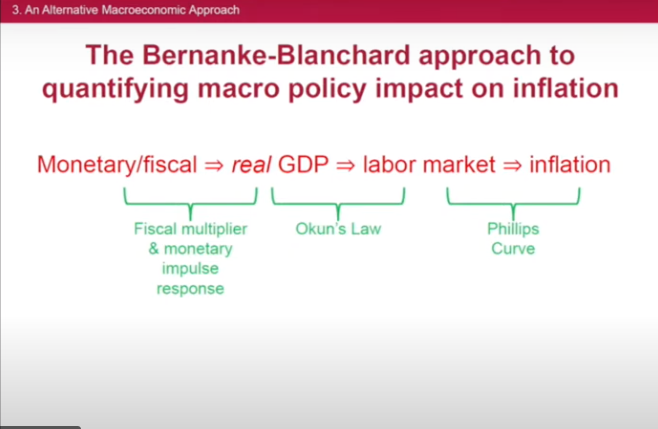

In his dialogue, Jason Furman offered a slide exhibiting his interpretation of their framework for combination demand shocks:

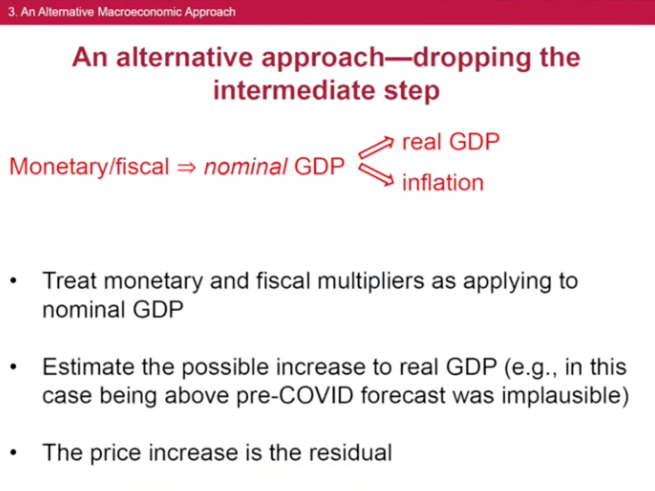

He contrasted that along with his most well-liked framework for the evaluation:

Very long time readers will acknowledge that that is additionally my most well-liked mind-set about demand shocks. By itself, actual GDP tells us nearly nothing about demand. In distinction, NGDP is an inexpensive proxy for combination demand. (That doesn’t cease pundits from sometimes citing actual output and/or actual consumption information as “demand,” though that’s an EC101-level error.)

Within the subsequent dialogue, Bernanke objected that the implications of rising NGDP had been ambiguous, as one may think about a state of affairs the place each the AS and AD curve shifted upward (much less AS, extra AD, no change in output.) Thus steady RGDP and rising NGDP doesn’t essentially indicate that the issue is primarily extra demand. He could have been reacting to this slide from Furman:

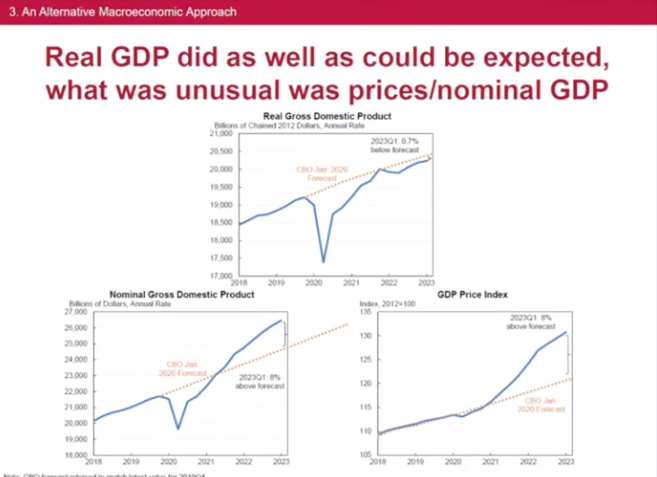

In an accounting sense, it seems just like the inflation drawback is 100% nominal, with actual GDP roughly on development. If I’m not mistaken, Bernanke’s argument is that in a counterfactual the place NGDP rose much less strongly, it’s potential that output would have been decrease (as a result of COVID, Ukraine, and many others.) and we nonetheless would have skilled some extra inflation (albeit presumably lower than what we truly skilled.)

Right here’s why I choose Furman’s method: Previous to COVID, unemployment was roughly 3.5%, and therefore the economic system was in all probability near equilibrium. In that case, we should always not have been aiming for quick NGDP development to scale back unemployment under 2019 ranges. Moderately, we should always have aimed for NGDP development of roughly 2% plus the Fed’s estimate of development RGDP development after 2019. The truth is, we received a pair trillion {dollars} in extra NGDP development, roughly 8% above development. It could be surprising if that type of fast development in nominal spending had not created excessive inflation, on condition that we had been already close to full employment in early 2020.

That doesn’t imply that Bernanke’s theoretical remark is wrong. Moderately, I’m suggesting that his level might be of restricted relevance for this specific episode. Maybe COVID decreased combination provide by 1% or 2% between early 2020 and right now, and the highly effective demand stimulus boosted output by a roughly equal quantity, leaving RGDP near development. If NGDP had grown at development, maybe output can be 1% or 2% decrease than present ranges.

What appears implausible is that the change in combination provide over the previous three years is something near the 8% overshoot of demand. That type of fast development in nominal spending just isn’t a mandatory situation for inflation (provide shocks also can enhance the CPI), however it appears to me that it’s fairly near a adequate situation for prime inflation within the absence of some type of really extraordinary enhance in combination provide.

So whereas Bernanke is correct that quick rising NGDP doesn’t definitively show that extra demand is the reason for the latest inflation overshoot, given believable estimates of shifts within the AS curve, it appears extremely possible that the 8% NGDP overshoot is by far an important reason behind excessive inflation.

Furman additionally made some excellent observations concerning the difficulties concerned in separating provide and demand shocks. For example, congestion on the ports looks as if a “provide drawback.” However most of this congestion was not attributable to a bodily drawback on the ports. In line with Furman, import volumes at US ports had been far increased in 2021 than in 2019. As an alternative, it was the terribly massive demand for items throughout 2021 (partly pushed by stimulus checks) that was inflicting congestion on the ports. So in a way even the “bottleneck” issues had been partly extra demand, though they appeared like a provide drawback. (Once more, Blanchard and Bernanke acknowledged this drawback of their paper.)

In EC101, we’re taught that P and Y, thought-about in isolation, inform us nothing about provide and demand shocks. NGDP is completely different. It measures costs occasions output, or complete nominal expenditure. Thus NGDP is a reasonably direct learn on combination demand. As an alternative of all types of sectors (meals, vitality, companies, labor, funding, durables, exports, and many others.), NGDP offers a easy and stylish mind-set about complete demand within the economic system.

Sure, the Fed doesn’t immediately goal NGDP. However there isn’t a believable interpretation of the Fed’s twin mandate the place—if ranging from equilibrium—it’s applicable to have NGDP development both far above 4% or far under 4%. In 2008-09, we went roughly 8% under development (which was then 5%), and prior to now three years we’ve gone roughly 8% above. When the deviations in NGDP are that giant, it’s cheap to say that the issue is primarily demand.

P.S. In fact, I favor NGDP concentrating on, which is another excuse to choose Furman’s framing of the difficulty. However I’d choose his method even when the Fed sticks to its present “twin mandate” method. As St. Louis Fed President Jim Bullard as soon as noticed, the implications of FAIT (if symmetrical) are fairly just like NGDP stage concentrating on.

{kind=link}